CG 20 10 Explained: The Ongoing Operations Endorsement Contractors Need

CG 20 10 Explained: The Ongoing Operations Endorsement Contractors Need

You just landed a new commercial project. The general contractor sends over the paperwork, and somewhere in the stack of documents is a request that might look unfamiliar: "Provide CG 20 10 endorsement naming us as additional insured." Before you can set foot on that job site, you need to understand what this means and make sure your insurance is set up correctly.

The CG 20 10 is the most commonly requested additional insured endorsement in the contracting industry. It's so routine that many contractors don't think twice about it, which can lead to problems when the details matter most. A claim gets denied, a contract requirement goes unmet, or coverage gaps appear exactly when protection is needed.

Understanding what the CG 20 10 actually does, what it doesn't do, and how it fits alongside other endorsements can help you stay compliant with contract requirements and protect your business relationships.

What Does the CG 20 10 Endorsement Do?

The CG 20 10 is an endorsement added to your Commercial General Liability (CGL) policy that extends coverage to a specifically named third party for liability arising from your ongoing operations. When you add a general contractor, project owner, or property manager as an additional insured using this form, they gain certain protections under your policy while your work is actively in progress.

Picture this scenario: An HVAC contractor is installing ductwork on a new retail space. While carrying equipment through the building, a worker accidentally damages a glass partition that had already been installed. The property owner sues the general contractor for the damage. Because the general contractor is listed as an additional insured on the HVAC contractor's policy using the CG 20 10, they can seek defense and indemnification through that policy.

The endorsement is issued by the Insurance Services Office (ISO) and modifies the "Who Is An Insured" section of your CGL policy. The additional insured receives coverage, but only for liability connected to work you perform for them at the designated location.

Why General Contractors and Project Owners Require the CG 20 10

When a general contractor hires subcontractors, they take on risk. If something goes wrong on the job site involving a subcontractor's work, the general contractor often gets named in the lawsuit regardless of who was actually at fault. Property owners face the same exposure when they hire contractors directly.

Requiring additional insured status transfers some of that risk back to the party doing the work. Instead of the general contractor fighting a lawsuit using only their own insurance, they can tap into the subcontractor's policy for defense costs and potential damages.

There's also a practical audit consideration. Most CGL policies undergo annual audits that look at payroll and subcontractor costs. If a general contractor uses uninsured subcontractors, those subcontractor costs often get added to the general contractor's own premium calculations. By requiring subcontractors to carry proper insurance and provide additional insured status, general contractors protect themselves from these audit surprises.

For subcontractors, providing the CG 20 10 is simply the cost of doing business on commercial projects. Without it, you won't get past the first round of contract negotiations.

The Critical Limitation: Ongoing Operations Only

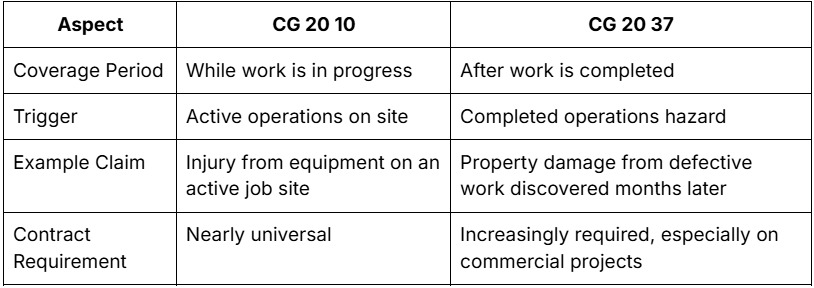

Here's where many contractors get tripped up. The CG 20 10 provides coverage for ongoing operations only. Once your work is complete, the protection it provides to the additional insured ends.

This wasn't always the case. Before 1985, the CG 20 10 endorsement covered both ongoing and completed operations under the phrase "liability arising out of your work." The term "your work" in insurance language includes both active operations and finished work. After the 1985 revision, ISO split these coverages apart, limiting the CG 20 10 to ongoing operations and creating the CG 20 37 for completed operations.

Why does this matter? Consider an electrical contractor who finishes wiring a commercial kitchen. Three months later, faulty wiring causes a fire. The restaurant owner sues the general contractor who built out the space. If the general contractor was only listed as an additional insured using the CG 20 10, they have no coverage under the electrical contractor's policy because the work was already complete.

To provide full protection to an additional insured, contractors typically need both the CG 20 10 for ongoing operations and the CG 20 37 for completed operations.

How the CG 20 10 Differs from the CG 20 37

These two endorsements work as a pair, but they cover completely different timeframes.

Think of it like a relay race. The CG 20 10 carries the baton while your crews are on site, and the CG 20 37 takes over once the work is done and accepted. Neither one provides complete coverage alone. Sophisticated project owners and general contractors understand this and require both endorsements in their contracts.

Version History and What It Means for Your Coverage

ISO periodically updates its endorsement forms, and the CG 20 10 has changed significantly over the years. Each version provides slightly different coverage, which matters when claims arise or when contracts specify particular edition dates.

CG 20 10 11/85

The broadest version ever issued. It covered additional insureds for liability "arising out of your work," which courts interpreted to include both ongoing and completed operations. Some contracts still request this version, though most carriers no longer offer it.

CG 20 10 10/01

This edition narrowed coverage to "ongoing operations" only, removing completed operations protection. However, it retained the "arising out of" language, which provided relatively broad coverage during the ongoing phase.

CG 20 10 07/04

ISO changed the trigger from "arising out of" to "caused, in whole or in part, by" the named insured's acts or omissions. This shift had major implications. Under the earlier language, courts often found coverage even when the additional insured was mostly or entirely at fault. The new language requires the named insured (the subcontractor) to bear at least some responsibility before the additional insured can access coverage.

CG 20 10 04/13 and 12/19

These current editions maintain the "caused, in whole or in part, by" language and add restrictions tied to contract requirements and legal limitations. Coverage applies only to the extent permitted by law, and when a written contract exists, the endorsement won't provide broader protection than the contract requires. The 12/19 version further clarifies that payment is limited to the lesser of what's contractually required or the available policy limits.

Meeting Contract Requirements: Scheduled vs. Blanket Coverage

Contractors can provide additional insured coverage in two ways, and understanding the difference can save time and prevent coverage gaps.

Scheduled endorsements like the CG 20 10 require you to specifically list each additional insured by name, along with project details and locations. Every time you start a new project with a new general contractor, you need to request an endorsement naming them.

Blanket or automatic endorsements (like the CG 20 33) provide additional insured status automatically to anyone you're contractually required to cover. You don't need to request a separate endorsement for each project because the coverage attaches automatically when a contract requires it.

The CG 20 33 is often more convenient for contractors who work with multiple general contractors throughout the year. However, it has one significant requirement that the CG 20 10 does not: a written contract must exist between you and the additional insured. If that contract isn't in place, or if it's verbal rather than written, the CG 20 33 won't provide coverage.

The CG 20 10 doesn't require a written contract. The additional insured just needs to be listed on the endorsement. This makes it more flexible in some situations but requires more administrative effort to maintain.

Common Misconceptions About the CG 20 10

Misconception: The CG 20 10 covers everything on the job site. Reality: It only covers liability arising from your specific operations for the additional insured. If damage involves another contractor's work or something unrelated to your operations, the endorsement doesn't respond.

Misconception: Being named as additional insured means they have primary coverage. Reality: Whether the additional insured's coverage is primary or excess depends on policy language and the underlying contract. The CG 20 10 itself doesn't determine priority of coverage.

Misconception: One CG 20 10 covers the additional insured forever. Reality: Coverage ends when your work is complete. For post-completion protection, the additional insured needs coverage under a CG 20 37.

Misconception: All CG 20 10 endorsements are the same. Reality: Different edition dates have different coverage triggers and limitations. A CG 20 10 04/13 provides narrower coverage than a CG 20 10 10/01.

Steps to Get Your Additional Insured Endorsements Right

Staying on top of additional insured requirements doesn't have to be complicated, but it does require a system.

Before signing contracts, review the insurance requirements section thoroughly. Note what endorsements are required, whether specific edition dates are mentioned, and how long coverage must remain in place.

Work with an experienced agent who understands contractor insurance. They should be able to issue endorsements quickly and explain what coverage you're actually providing. Ask them to confirm in writing that your policy includes both the CG 20 10 and CG 20 37 endorsements.

Request certificates of insurance that specifically reference the additional insured endorsements. A certificate alone doesn't prove coverage, but it should accurately reflect what endorsements are attached to your policy.

Keep organized records of all certificates, endorsements, and contracts for every project. Claims can surface years after work is completed, and you'll need documentation proving what coverage was in place.

Communicate with your insurance team before every new project. If you're working with a new general contractor, let your agent know so they can issue the appropriate endorsements promptly.

Protecting Your Business and Your Relationships

The CG 20 10 endorsement is a fundamental part of how risk gets allocated on construction projects. By providing this coverage to general contractors and project owners, you're demonstrating professionalism and making it easier for them to work with you. It's an expectation on virtually every commercial project, and having it in place before it's needed keeps your projects moving smoothly.

If you have questions about your current additional insured coverage or need help securing the right endorsements for an upcoming project, Contractor Coverage specializes in exactly these situations. With over 20 years of experience and access to more than 200 carriers, we can find solutions that meet your contractual requirements and keep your business protected. Reach out for a quote or give us a call to discuss your needs.